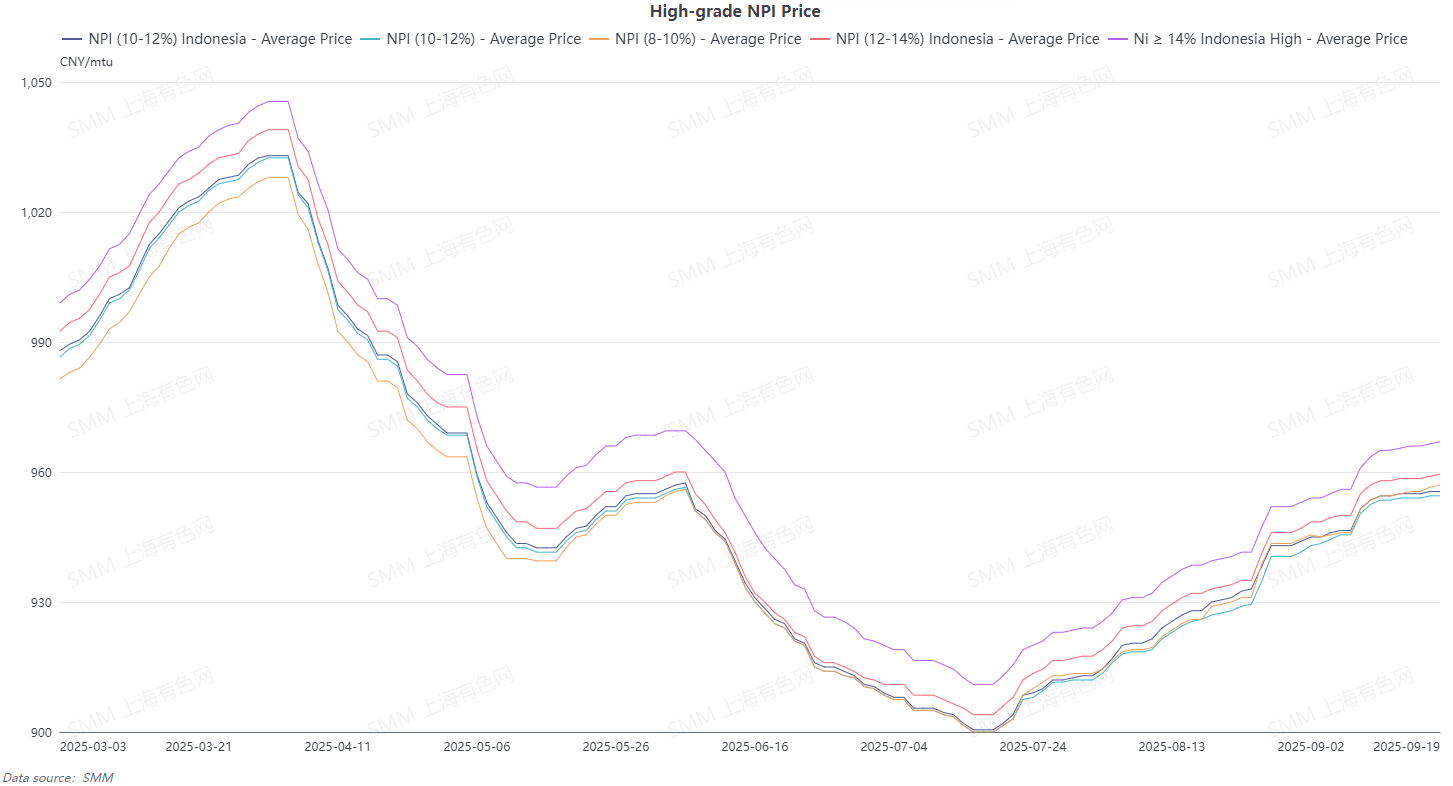

The average price of SMM 10-12% high-grade NPI rose WoW by 3.1 yuan/mtu to 954.2 yuan/mtu (ex-factory, tax included), while the Indonesian NPI FOB index price increased WoW by $0.54/mtu to $117.44/mtu. High-grade NPI prices maintained an upward trend this week, but the momentum noticeably slowed down.

Supply side, supported by the traditional peak season, social inventory of stainless steel continues destocking, while auxiliary material prices rebound, providing more pronounced support for domestic cost lines, and smelters maintain reluctance to budge on prices. Demand side, although social inventory of stainless steel continues destocking, it is difficult for the selling price of stainless steel finished products to recover; both production and consumption of 300-series stainless steel fall short of expectations. Overall costs for stainless steel enterprises rise, while there is no optimistic outlook for October consumption, exerting pressure on high-grade NPI prices. Overall, end-use consumption growth remains slow, and consumption of 300-series stainless steel significantly underperforms expectations, hindering the rise of high-grade NPI. However, supported by cost factors and the peak season, high-grade NPI prices remain firm and are expected to maintain a sideways movement at high levels next week.

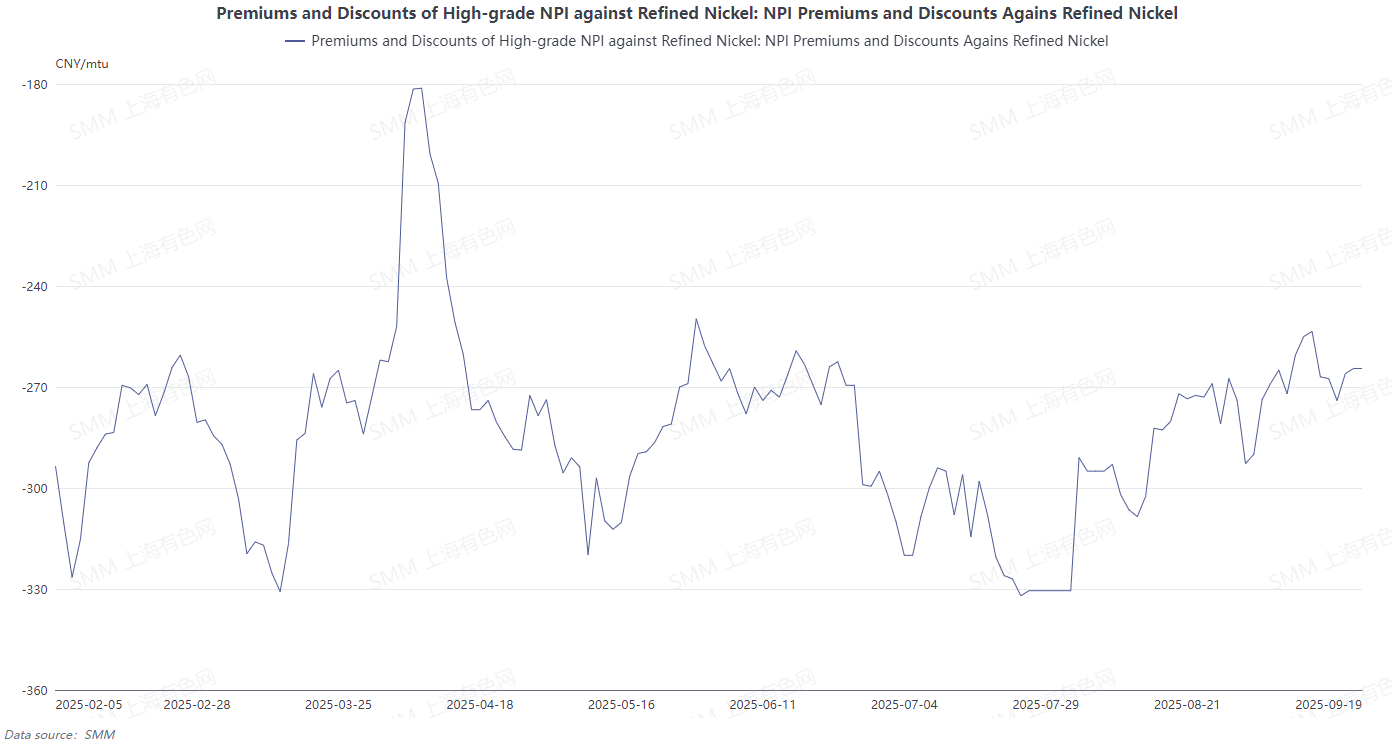

From the perspective of NPI conversion to high-grade nickel matte, nickel prices averaged higher this week amid the US Fed interest rate cut, while high-grade NPI prices rose slowly. The average discount of high-grade NPI to refined nickel widened to 267.3 yuan/mt this week. Refined nickel prices are expected to remain flat next week, and high-grade NPI prices are also projected to hover at highs. The average discount of high-grade NPI to refined nickel may only experience minor fluctuations. Moreover, the current incentive for converting high-grade NPI to high-grade nickel matte is weak, and the proportion of NPI conversion to high-grade nickel matte is expected to be limited.

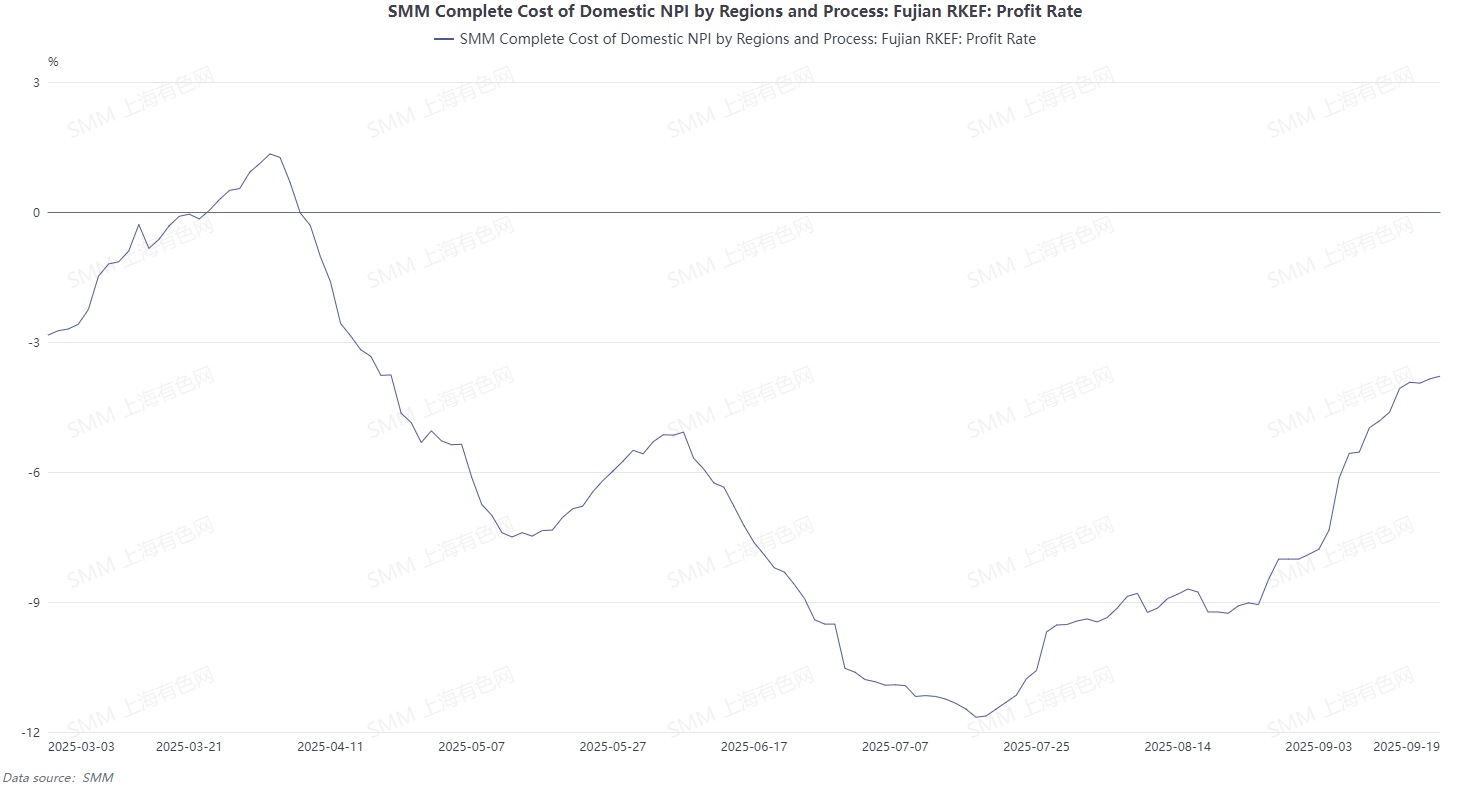

Cost side, based on nickel ore prices 25 days ago, smelter profits for high-grade NPI remained in negative territory this week. Raw material side, ore prices held steady, while coking coal and coke prices rebounded significantly, supporting a firm cost line. Meanwhile, high-grade NPI prices faced upward resistance. Looking ahead to next week, auxiliary material prices are expected to remain elevated, and ore prices are also projected to hold steady. Against the backdrop of pressure on high-grade NPI prices, smelter profits are expected to face a renewed risk of decline.